CLICK HERE Présentation L’Association Internationale de Droit de la Consommation et le Laboratoire Innovation Communication et Marché se sont associés pour ce congrès européen de droit de la consommation qui se tiendra à Montpellier les 27 et 28 février 2025. Accueillant des chercheurs et praticiens du monde entier, représentant 18 nationalités, il est l’occasion de […]

The annual Australasian Consumer Law Roundtable will be hosted this year by the Centre for Law as Protection at Deakin Law School on 5-6 December 2024. International Association of Consumer Law (IACL) is co-badging our second day, the 6 December, as the IACL Regional Meeting. Event details Day/Time: 5-6 Dec 2024 Venue: Deakin Law School Please note: Only […]

Under the theme "New challenges in consumer law: celebrating 40 years of the United Nations Guidelines for Consumer Protection and the Founding Fathers of IACL," the conference will address advances and pending challenges in consumer rights protection. The Faculty of Law at the University of Buenos Aires will host the 19th Conference of the International […]

Topic: “40 years of United Nations Guidelines for Consumer Protection: Impacts and challenges” Abstract submission deadline: 31 January 2025 Feedback: 24 February 2023 Guidelines: max. 300 words, 5-7 keywords Dates: 23, 24 and 25 July 2025 Venue: Facultad de Derecho de la Universidad de Buenos Aires (English and Spanish sessions) and Facultad de Ciencias Jurídicas […]

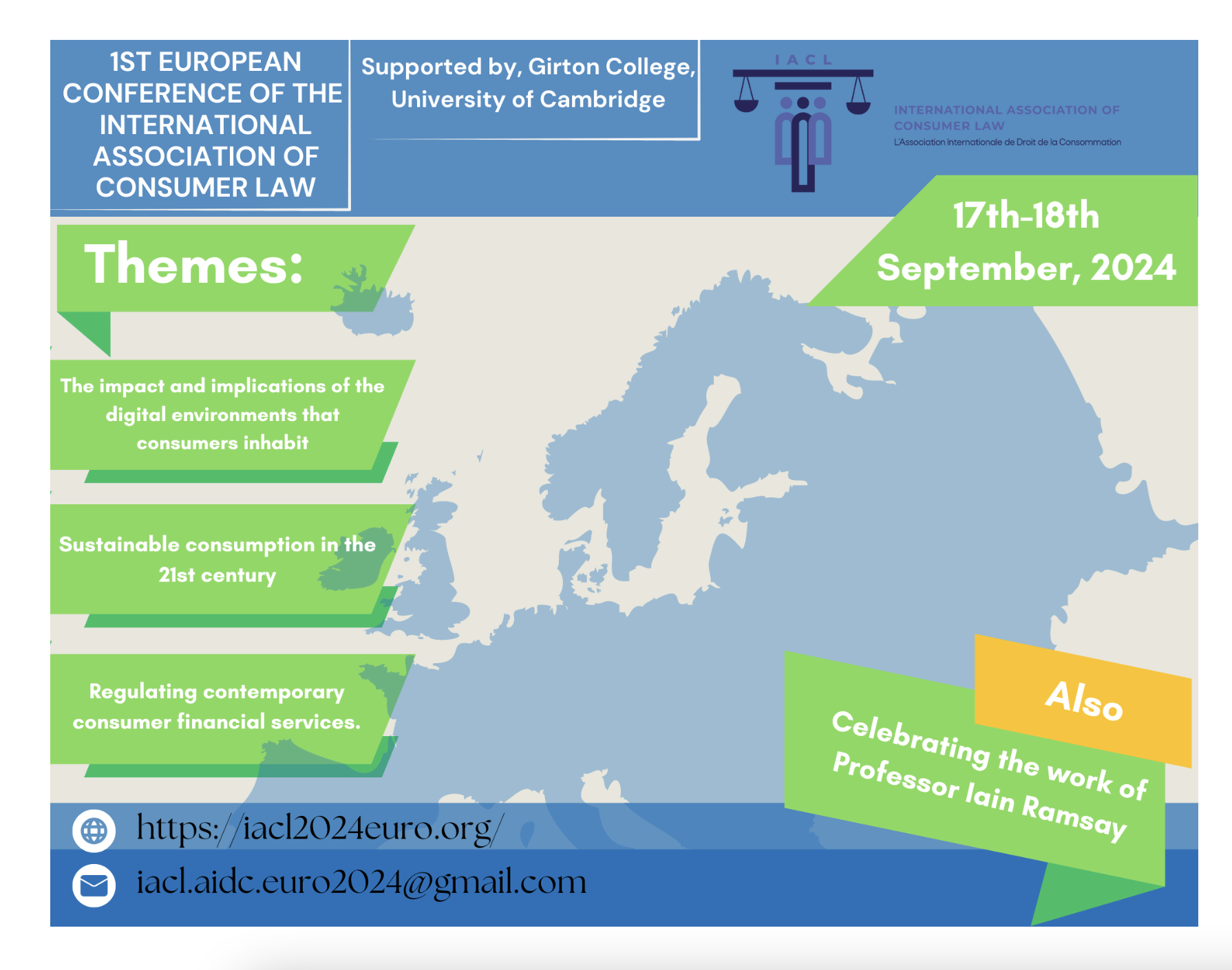

1st European conference of the International Association of Consumer Law Welcome to the First European Regional conference of the International Association of Consumer Law-L'Association Internationale de droit de la consommation (IACL-Europe)! Join us at Girton College, University of Cambridge for two days filled with insightful discussions, networking opportunities, and engaging presentations. This in-person event is a fantastic […]

Event: International Association of Consumer Law (IACL) Regional Meeting, 6 Dec 2024, Deakin Law School, Melbourne, Australia Date: Friday, 6 December 2024 Location: Deakin Downtown, Level 12, Tower 2727 Collins Street Melbourne, VIC, 3008 Australia Dear colleagues, We are hosting the IACL Regional Meeting at Deakin Law School, Deakin Downtown campus, Melbourne, Australia on 6 December 2024. The event is […]

CALL FOR PAPERS Global challenges for consumer law and policy in contemporary Europe 1st European conference of the International Association of Consumer Law (IACL) 17-18 September, Girton College Cambridge (UK) and honouring the work of Prof. Iain Ramsay The Board Members of the International Association of Consumer Law/Association Internationale de Droit de la Consommation […]

Berk/ELI Transatlantic Conversation on Consumer Protection Law Wednesday, April 3 8:00 a.m. PDT / 17:00 CEST The UC Berkeley Center for Consumer Law & Economic Justice and the European Law Institute Digital Law SIG are pleased to invite you to the next conversation in a series of transatlantic conversations on pressing issues in the area of consumer protection law. […]

“Teaching Consumer Law in a Changing Environment” Santa Fe, New Mexico May 17-18, 2024 Preceded by the Law School Consumer Clinic Conference on May 16 The Center for Consumer Law & Economic Justice at the UC Berkeley School of Law and The Center for Consumer Law at the University of Houston Law Center are […]

“Teaching Consumer Law in a Changing Environment” Santa Fe, New Mexico May 17 & 18, 2024 Special supplemental session for clinical faculty, May 16. The Center for Consumer Law & Economic Justice at the UC Berkeley School of Law and The Center for Consumer Law at the University of Houston Law Center are proud to […]

Recent Comments